If you’re a civil construction SME chasing NSW Government work, your financial assessment will determine what contracts you can bid on — and a single misstep on your balance sheet can lock you out. The Buy.NSW Financial Assessment Services Scheme (SCM2491) is the mandatory whole-of-government mechanism through which NSW Treasury evaluates whether contractors have the financial capacity to deliver public construction projects.[1] For SMEs operating in the $50K–$2M range, understanding how financial assessments work, what metrics matter, and how to prepare your business isn’t optional — it’s the difference between winning government work and watching it go to your competitors.

At TenderBuilt, we help civil construction businesses across NSW, Queensland, and Victoria navigate government prequalification every day. We’ve seen contractors denied prequalification because of undocumented director loans, watched businesses get assessed two financial levels below their actual operating capacity because of poor balance sheet timing, and helped SMEs restructure their finances to unlock hundreds of thousands of dollars in additional contract capacity. This guide distils everything we’ve learned into a single, practical resource.

1. What the Financial Assessment Services Scheme actually does

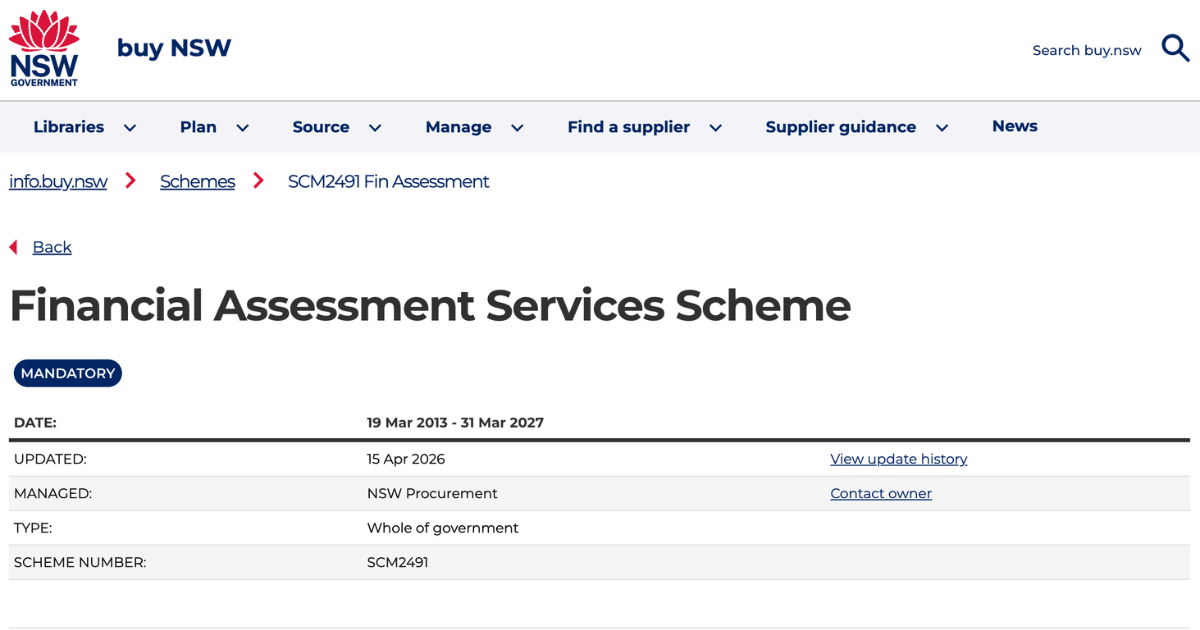

The Financial Assessment Services Scheme (SCM2491) is not itself a construction prequalification scheme. Rather, it is a panel of 13 prequalified financial assessment firms that NSW Government agencies must use when evaluating a contractor’s financial capacity to deliver construction work.[1] The scheme was established on 19 March 2013, is managed by NSW Procurement within NSW Treasury, and operates under the authority of Procurement Board Direction PBD-2013-01C, which was issued on 13 November 2013, took effect on 1 January 2014, and was extended indefinitely on 30 March 2016.[2]

The scheme serves three distinct purposes across the procurement lifecycle. First, it supports prequalification — assessing whether a contractor meets financial capacity thresholds for inclusion on government supplier panels. Second, it enables tender-stage assessment — evaluating the financial risk of awarding a specific contract to a specific contractor. Third, it facilitates ongoing monitoring — rolling financial assessments throughout the life of active construction contracts to catch deteriorating contractor finances before a project collapses.[2]

NSW Procurement maintains a Central Repository of financial assessment reports at Treasury, accessible by all government agencies. This repository eliminates duplicate assessments: if an agency has already commissioned a financial assessment on your business, another agency can access that existing report rather than commissioning a new one. Agencies can request access by emailing financialassessments@treasury.nsw.gov.au.[1]

The scheme is classified as a mandatory whole-of-government arrangement under PBD 2021-04 (Approved Procurement Arrangements), meaning agencies cannot engage external financial assessors for construction procurement outside this panel unless they conduct assessments internally.[3]

2. Three tiers of construction prequalification and their financial requirements

NSW Government construction prequalification operates across three distinct tiers, all managed by NSW Public Works through the Buy.NSW Supplier Hub. The financial assessment requirements escalate significantly as contract values increase, and understanding which tier applies to your business is the critical first step.[4]

SCM0256 — General construction works up to $1 million

This is the entry-level scheme and the most relevant for small civil construction businesses. It subdivides into two categories: Registered suppliers (engagement fees up to $250,000 excluding GST) and Certified suppliers ($250,000 to $1 million, requiring at least two years of ASIC-registered trading history in Australia).[5] The scheme is mandatory under PBD-2014-04C, covering 22-plus work categories including the C5 Civil Works category — which covers bulk earthwork, excavation, road work, car parks, trenching, pipe laying, and small water and sewerage treatment plants.[6]

Critically for SMEs, no formal financial assessment from the SCM2491 panel is conducted at the prequalification stage for this tier — applicants need only self-certify that the business can pay all debts when due. However, agencies may require an independent financial assessment before awarding specific contracts, so financial readiness still matters even at this lowest level.[5]

SCM1461 — Contractor prequalification $1M–$9M

This scheme covers construction work valued between $1 million and $9 million (excluding GST) across categories including building works, civil works, water infrastructure, wastewater infrastructure, heritage, and demolition.[7] Financial capacity is formally assessed as one of four prequalification criteria (alongside legal capacity, commercial ability, and technical ability). Updated scheme conditions were published in December 2024, and the scheme runs until 31 December 2028. This tier requires ISO 45001 (WHS) and ISO 9001 (quality) certification.[8]

SCM100002 — Procurement List for construction services over $9 million

This tier carries the most rigorous financial requirements. Subject to Enforceable Procurement Provisions (PBD-2019-05), contractors must upload two years of annual financial statements complying with recognised accounting standards (IFRS, US-GAAP, or AASB). An external financial assessor from the SCM2491 panel contacts the supplier directly to conduct the assessment on behalf of government.[9] Contractors must demonstrate a Current Ratio greater than 1.0, undergo annual financial viability checks, and submit annual reporting. This tier also uniquely requires ISO 14001 environmental management certification in addition to ISO 45001 and ISO 9001.[9]

| Scheme | Contract value | Financial assessment | ISO requirements |

|---|---|---|---|

| SCM0256 — Registered | Up to $250K | Self-certification only | None (WHS evidence required) |

| SCM0256 — Certified | $250K–$1M | Self-certification; agency may request formal assessment pre-award | None (WHS evidence required) |

| SCM1461 | $1M–$9M | Formal assessment by designated assessor | ISO 45001, ISO 9001 |

| SCM100002 | Over $9M | SCM2491 panel assessor; annual viability checks; Current Ratio >1.0 | ISO 45001, ISO 9001, ISO 14001 |

3. The financial assessment methodology: formulas that determine your contract capacity

The most detailed and authoritative documentation of the financial assessment methodology comes from the Transport for NSW NPS Guidelines (Edition 2, Revision 9, November 2025), which implements the Austroads National Prequalification System for civil road and bridge construction.[10] While this methodology applies specifically to TfNSW contracts, the same principles and formulas are applied by SCM2491 panel assessors across all NSW Government construction procurement.

The assessment follows a four-step process documented in Appendix B (Criteria 4) of the TfNSW NPS Guidelines.[10]

Step 1 — Preliminary contract capacity

The starting calculation is straightforward: preliminary contract capacity equals 5 times assessed working capital. Working capital is calculated as current assets minus current liabilities from the entity’s balance sheet. For a civil contractor with $400,000 in working capital, the preliminary capacity would be $2 million. Assessors require satisfactory evidence of the collectability of any related-entity loans included in current assets.[10]

Step 2 — Risk overlays

Two hard constraints may reduce the preliminary capacity. The NTA cap limits preliminary contract capacity to no more than 12.5 times Net Tangible Assets (where NTA equals total assets minus intangible assets minus total liabilities). The Quick Ratio must be at least 0.8 (calculated as current assets minus inventory, divided by current liabilities). Falling below this threshold can disqualify a contractor entirely.[11] These overlays mean that even if your working capital looks strong, inadequate NTA or poor liquidity can dramatically reduce your assessed capacity.

Step 3 — Qualitative adjustment

This is where professional judgment enters the equation, and where experienced assessors can materially increase or decrease a contractor’s assessed level. The TfNSW guidelines list 16 qualitative factors including governance quality, accounting policies, age of business, aging of debtors and creditors, registered charges against the business, length of banking relationships, current contracts on hand, budgets and cash flow projections, debt-to-equity ratio (benchmarked against a 60/40 split — 60% debt to 40% equity), revenue trends over three years, profitability after tax over three years, quality of financial statements, and availability of credit lines.[10]

Upward adjustments of more than one financial level must be flagged with an asterisk — for example, a contractor whose quantitative assessment places them at F5 but who receives an upward adjustment to F25 would be recorded as F25*.[10]

Step 4 — Final assessed capacity

The assessed contract capacity represents the maximum additional aggregate contract cash flow commitment over a 12-month period, assuming a relatively even spread of cash flow. This is expressed as a financial level (F-level) that determines the maximum contract value the contractor can bid for.[11]

The formula in plain English: Start with 5 × your working capital. Check that this doesn’t exceed 12.5 × your net tangible assets. Confirm your Quick Ratio is at least 0.8. Then the assessor adjusts up or down based on 16 qualitative factors. The result is your F-level — the maximum contract value you can bid for.

4. Austroads NPS financial levels from F0.25 to F150+

The Austroads National Prequalification System uses 13 financial levels identified by the letter “F”, each representing a maximum contract value (including GST) a contractor may tender for. These levels are used across all Australian states and territories that participate in the NPS, with mutual recognition agreements allowing contractors prequalified in one jurisdiction to seek recognition in others.[11]

| Financial level | Maximum contract value (inc. GST) | Approx. working capital needed |

|---|---|---|

| F0.25 | $250,000 | ~$50,000 |

| F1 | $1 million | ~$200,000 |

| F2 | $2 million | ~$400,000 |

| F5 | $5 million | ~$1 million |

| F10 | $10 million | ~$2 million |

| F15 | $15 million | ~$3 million |

| F20 | $20 million | ~$4 million |

| F25 | $25 million | ~$5 million |

| F50 | $50 million | ~$10 million |

| F75 | $75 million | ~$15 million |

| F100 | $100 million | ~$20 million |

| F150 | $150 million | ~$30 million |

| F150 PLUS | Unlimited | Assessed individually |

The levels F0.25, F1, and F2 are optional — not all jurisdictions use them. NSW through TfNSW does recognise these lower levels, while Queensland TMR does not recognise F0.25.[12]

For the typical civil construction SME targeting contracts in the $50K–$2M range, the relevant financial levels are F0.25 through F2. The approximate working capital figures in the table above are starting points based on the 5× formula — qualitative adjustments, NTA caps, and Quick Ratio constraints can shift the final result in either direction.

TfNSW mandates prequalification for all civil construction contracts exceeding $250,000 (excluding GST) and requires an updated financial assessment within the preceding six months before awarding any contract.[10] Local Government Councils are automatically granted F5 without financial assessment, and Aboriginal businesses with 50% or greater Aboriginal ownership may be exempted from financial assessment and assigned a base level of F0.25.[10]

5. The 13 approved financial assessors and how the process works

A common misconception among contractors is that they choose their own financial assessor. The contractor does not select the assessor. The NSW Government agency commissioning the work engages an assessor from the SCM2491 panel, and that assessor then contacts the contractor to request financial information. The agency bears the cost of the assessment — though for TfNSW NPS prequalification, costs may be borne by the contractor.[1]

The 13 firms currently approved on the panel span major accounting firms, specialist advisory practices, and credit rating agencies:[1]

| Assessor firm | Assessment levels | Specialisation |

|---|---|---|

| Deloitte Touche Tohmatsu | Basic, Medium, Comprehensive | Big 4 accounting |

| Equifax Australasia Credit Ratings | Basic, Medium, Comprehensive | Credit ratings; online portal for agencies |

| Ernst & Young | Basic, Medium, Comprehensive | Big 4 accounting |

| KPMG | Basic, Medium, Comprehensive | Big 4 accounting |

| Vincents Chartered Accountants | Basic, Medium, Comprehensive | Multi-state panels (VIC, QLD, Cwlth, ACT, NT) |

| Newpoint Advisory | Basic, Medium, Comprehensive | Property and construction risk |

| Paxon Consulting Group | Basic, Medium, Comprehensive | Infrastructure and commercial advisory |

| Olvera Advisory | Basic, Medium, Comprehensive | Counterparty assessments; related-party analysis |

| Financial and Commercial Advisory | Basic, Medium, Comprehensive | Government financial advisory |

| Fiable Pty Ltd | Basic, Medium only | SME-focused assessments |

| McGrathNichol Advisory Partners | Comprehensive only | Restructuring and insolvency |

| O’Connor Marsden & Associates | Basic only | Risk advisory |

| Illion Australia | Basic only | Credit and risk data |

Assessment fees are not publicly disclosed. Equifax explicitly states that tendered rates are confidential.[13] Fees are structured as a fixed fee per report, varying by assessment type and turnaround time. Three report types are available: Basic (5 working days standard, 3 priority), Medium (7 days standard, 4 priority), and Comprehensive (10 days standard, 5 priority).[1]

The recommended report type depends on contract value — Basic for contracts under $1 million, Medium for contracts under $10 million, and Comprehensive for contracts exceeding $10 million.[2]

6. The Guide to Financial Assessment Reports

NSW Treasury publishes a key companion document titled the “Guide to Financial Assessment Reports” on the scheme page at info.buy.nsw.gov.au/schemes/financial-assessment-services-scheme.[1] The guide was last updated on 1 July 2019 and is available as a DOCX file (914 KB). It contains a worked example of a Medium Assessment and is the primary reference for government agencies interpreting financial assessment reports.

The guide is designed for agency procurement officers rather than contractors, but it is invaluable reading for any construction business seeking to understand exactly what assessors report on and how agencies interpret the results. It walks through each section of a standard financial assessment report including the executive summary and overall rating, balance sheet analysis, profitability trends, liquidity ratios, working capital adequacy, NTA assessment, and the assessor’s recommended contract capacity with any qualitative adjustments noted.

Additional supporting documents published on the scheme page include:[1]

- Guidelines for Agencies (March 2022) — how to order, interpret, and act on financial assessments

- Guidelines for Applicants (March 2022) — what contractors should expect and what documents to have ready

- Assessment report templates for Basic, Medium, and Comprehensive levels

- Order Form (most recently updated May 2025) — the form agencies use to commission assessments from panel firms

- Monthly reporting template (Version 1.8, February 2025) — for rolling assessments during contract delivery

- Central Repository list (updated 13 April 2026) — register of existing assessment reports available to agencies

Tip for contractors: Request a copy of the “Guidelines for Applicants” document from the scheme page before your first financial assessment. It sets out exactly what information the assessor will request, what format it should be in, and what common issues delay the process. Being prepared with clean, well-organised financial documents can reduce assessment turnaround from weeks to days.

7. Rolling assessments and PBD-2013-01C requirements during contract delivery

Winning a contract doesn’t end the financial scrutiny. PBD-2013-01C mandates rolling financial assessments throughout the life of government construction contracts, with frequency tied to contract value.[2]

| Contract value | Assessment frequency | Maximum report age |

|---|---|---|

| $1M–$10M | Minimum 6-monthly | 6 months at time of use |

| Over $10M | Minimum 3-monthly | 3 months at time of use |

Agencies must also verify head contractor claims regarding payments to subcontractors — a provision that gained prominence after high-profile contractor insolvencies left subcontractors unpaid on major government projects. Any risks identified in financial assessment reports must be addressed through documented mitigation strategies.[2] These requirements apply to all NSW Government construction contracts above $1 million, regardless of which prequalification scheme the contractor entered through.

For contractors, this means your financial position is under continuous scrutiny once you win government work. A deterioration in your financial metrics mid-contract — caused by a bad debtor, an equipment purchase funded by short-term debt, or a large distribution to owners — can trigger risk flags that lead to enhanced monitoring, additional security requirements, or in extreme cases, contract termination. Maintaining consistent financial health throughout a contract is as important as demonstrating it at the prequalification stage.

8. How trust structures, director loans, and related-party transactions affect your assessment

For the majority of Australian construction SMEs that operate through family trusts or corporate trustees, the financial assessment process creates structural challenges that require careful planning.

Trust structures

Trusts face a fundamental disadvantage. Under NSW construction prequalification rules, trusts are not eligible for inclusion on schemes directly — applications must be lodged by the Trustee entity (for example, “ABC Pty Ltd ATF The Smith Family Trust”). The ABN of the Trust and ACN of the Trustee must both be provided.[6] The financial assessment then evaluates the trustee entity’s financial position, not the trust’s. Since trustee companies typically hold minimal assets in their own right — with the substantive business assets sitting in the trust — this can produce an NTA figure far lower than the economic reality of the business. Trust assets are generally excluded from NTA calculations, while trust liabilities incurred by the trustee may still be counted against it.[14]

Unpaid present entitlements (UPEs) require evidence of prior-year distributions and formal resolution documentation to be recognised as current assets. Without this documentation, UPEs are typically excluded — effectively reducing both working capital and NTA simultaneously.

Director loans — the single most common problem

Director loans are the single most common issue that undermines SME financial assessments. When a director withdraws cash from the company — whether for personal use, property investment, or other purposes — this creates a related-party receivable that assessors typically scrutinise heavily.[10]

Under the Austroads NPS guidelines, satisfactory evidence of the collectability of related-entity loans must be provided for these amounts to be included in working capital calculations. In practice, many assessors disallow director loans from NTA calculations unless strict documentation requirements are met, including formal loan agreements, repayment schedules, and evidence of actual repayments. Director loans simultaneously reduce working capital (cash leaves the business) and may not count as recoverable assets, creating a double penalty. They also trigger Division 7A of the Tax Act if not properly documented, creating additional compliance risks.[15]

Related-party transactions

Related-party transactions receive close scrutiny across all assessment levels. Olvera Advisory, one of the panel assessors, explicitly notes that their assessments include analysis of financial performance and liquidity with consideration to any related-party transactions such as intra-group loans.[16] Inter-company arrangements including loans and current contractual commitments are factored into assessments. Transactions must be at arm’s length and well-documented to avoid negative adjustment.

9. Practical steps SMEs should take before a financial assessment

Construction businesses in the $50K–$2M range can take concrete actions to strengthen their financial position before an assessment. Based on the assessment methodology and the 16 qualitative factors assessors consider, the most impactful steps are:

Start preparing 6–12 months early

Financial assessments use your most recent balance sheet, so the structure of your balance sheet at year-end (or the reporting date closest to assessment) directly determines your assessed capacity. Strategic timing of expenses, debt repayments, and capital transactions can materially affect the result.

Eliminate or formalise director loans

This is the highest-impact action for most SMEs. Repay director loans before the balance sheet date, or at minimum ensure they are supported by formal loan agreements with documented repayment schedules and evidence of actual repayments. Converting director loans to equity (through formal capitalisation) removes them from the equation entirely and strengthens NTA.[15]

Convert short-term debt to long-term facilities

Reclassifying current liabilities as non-current liabilities directly increases working capital without changing the total debt position. Refinancing short-term borrowings into facilities with terms exceeding 12 months shifts them out of the current liabilities calculation, immediately improving your 5× working capital figure.

Retain earnings rather than distributing

For trust structures in particular, large discretionary distributions immediately before a financial assessment strip working capital from the assessed entity. Consider the timing and quantum of distributions relative to upcoming assessments.

Secure documented credit facilities

Even unused credit lines can positively influence the qualitative assessment if evidenced by unconditional bank facility approval letters. The TfNSW guidelines specifically list availability of credit lines as one of the 16 qualitative factors.[10]

Maintain clean payment records

Assessors check trade supplier and subcontractor payment histories, and consistently late payments signal financial distress. Maintain current payments to key suppliers and subcontractors in the months leading up to assessment.

Invest in quality financial statements

Audited financial statements carry significantly more weight than compilation reports or management accounts in the qualitative assessment. While audits are expensive for SMEs, at minimum engage a qualified accountant to prepare reviewed financial statements that comply with Australian Accounting Standards. For contracts above $10 million, audited statements become effectively mandatory.[10]

10. What changed in 2024–2026 and what to watch

Several significant procurement reforms have reshaped the landscape since 2024, and contractors need to understand how these changes affect financial assessment requirements.

Mandatory Buy.NSW registration (1 July 2024)

PBD-2023-04 mandated registration of all NSW Government suppliers on the Buy.NSW Supplier Hub from 1 July 2024 — including contractors prequalified under the TfNSW NPS for civil construction. If you haven’t registered, you cannot be considered for government work.[17]

NSW Procurement Policy Framework update (December 2024)

The framework received a comprehensive update consolidating all current policy settings. PBD 2024-02 introduced local market testing requirements for procurements above $7.5 million, requiring agencies to check for capable NSW-based suppliers and justify awarding to out-of-state contractors — a measure that favours NSW-based SMEs.[18] Amendments to the Enforceable Procurement Provisions in October 2024 removed prohibitions on local content requirements, giving agencies more flexibility to favour local products and suppliers.

SME-specific thresholds

PBD-2023-03 raised the threshold for direct negotiation with small businesses to $250,000, and PBD-2019-03 requires agencies to seek at least one SME quote for competitive construction processes up to $1 million.[19] For smaller civil contractors, these provisions create opportunities to win work without requiring a formal financial assessment at all — provided you are registered on Buy.NSW and hold SCM0256 prequalification.

Scheme-specific updates

Within the Financial Assessment Services Scheme itself, the Order Form was updated in May 2025, the monthly reporting template reached version 1.8 in February 2025, and the SCM1461 scheme conditions were updated in December 2024.[1] The Austroads NPS was updated to the 2025 Edition (Revision 9, November 2025).[10] PBD 2024-01 mandated publication of all procurement opportunities above $150,000 on the Buy.NSW Tenders module by 31 December 2025, increasing visibility for SMEs.[18]

Construction law reform

The NSW Government’s proposed Building Bill 2024, which would have consolidated nine construction-related acts, was shelved in favour of targeted Building Productivity Reforms.[20] While this does not directly affect the financial assessment scheme, contractors should monitor reform progress as future changes could alter prequalification requirements or financial assessment thresholds.

Conclusion

The Buy.NSW Financial Assessment Services Scheme is ultimately a risk-management mechanism — government protecting itself from contractor insolvency on public projects. For SMEs, the practical implication is clear: your balance sheet is your tender qualification.

The 5× working capital formula, the 12.5× NTA cap, and the 0.8 Quick Ratio threshold are not abstract financial concepts — they are the precise calculations that determine whether you can bid on a $500,000 civil works contract or a $2 million road project. And unlike technical capability, which takes years to build, financial capacity can often be materially improved in a single financial year through deliberate balance sheet management.

The most actionable insight for SMEs in the $50K–$2M range is that financial assessment preparation is fundamentally a balance sheet management exercise, not an accounting compliance task. Director loans, trust distributions, short-term debt structures, and undocumented related-party transactions are the specific issues that most commonly reduce assessed capacity below a contractor’s actual operational capability. Addressing these 6–12 months before seeking prequalification — or before an agency commissions a pre-award assessment — is the single most effective step a civil construction SME can take to expand its government contracting opportunities in NSW.

References

- Financial Assessment Services Scheme (SCM2491) — info.buy.nsw.gov.au/schemes/financial-assessment-services-scheme. Scheme established 19 March 2013, managed by NSW Procurement (NSW Treasury). Lists 13 approved assessor firms, supporting documents, and Central Repository details. ↩

- Procurement Board Direction PBD-2013-01C — Financial Assessments — arp.nsw.gov.au. Issued 13 November 2013, effective 1 January 2014, extended indefinitely 30 March 2016. Mandates use of SCM2491 panel assessors and rolling assessments during contract delivery. ↩

- Procurement Board Direction PBD 2021-04 — Approved Procurement Arrangements — arp.nsw.gov.au. Classifies Financial Assessment Services Scheme as mandatory whole-of-government. ↩

- NSW Government construction prequalification schemes and procurement lists — publicworks.nsw.gov.au. Overview of all NSW construction prequalification tiers managed by NSW Public Works. ↩

- Construction Scheme for Works up to $1 Million (SCM0256) — info.buy.nsw.gov.au/schemes/construction-up-to-1M. Covers Registered (up to $250K) and Certified ($250K–$1M) tiers. Mandatory under PBD-2014-04C. ↩

- Department of Regional NSW Construction Prequalification Scheme — SCM0256 Applicant Guidelines, January 2024 — info.buy.nsw.gov.au (PDF). Details C5 Civil Works category, trust entity application requirements, and financial self-certification provisions. ↩

- Construction Scheme for Works between $1 Million and $9 Million (SCM1461) — info.buy.nsw.gov.au/schemes/construction-general-works-over-1M. Covers civil works, building works, water and wastewater infrastructure. Scheme runs until 31 December 2028. ↩

- SCM1461 Scheme Conditions, December 2024 — info.buy.nsw.gov.au (PDF). Requires ISO 45001 and ISO 9001 certification. ISO 14001 not required at this tier. ↩

- SCM100002 — Procurement List for Construction Services valued over $9 million — buy.nsw.gov.au. Requires two years of IFRS/US-GAAP/AASB-compliant financial statements, Current Ratio >1.0, annual viability checks, and ISO 14001 environmental certification. ↩

- Transport for NSW — National Prequalification System for Civil (Road and Bridge) Construction Contracts — Guidelines, Edition 2, Revision 9, November 2025 — transport.nsw.gov.au (PDF). Appendix B (Criteria 4) details the four-step financial assessment methodology, 16 qualitative factors, and F-level assignment process. ↩

- Austroads — Financial Levels — austroads.gov.au. Defines the 13 financial levels from F0.25 ($250,000) to F150 PLUS (unlimited). Includes the 5× working capital formula, 12.5× NTA cap, and 0.8 Quick Ratio threshold. ↩

- Austroads — Categories and Levels — austroads.gov.au. Notes that F0.25, F1, and F2 are optional levels not used by all jurisdictions. Queensland TMR does not recognise F0.25. ↩

- Equifax — NSW Government Financial Assessment Services Prequalification Scheme — equifax.com.au. Notes tendered rates are confidential. Describes the three assessment levels (Basic, Medium, Comprehensive) and the online portal for agencies. ↩

- Queensland Building and Construction Commission — Net Tangible Assets — qbcc.qld.gov.au. While QLD-specific, the QBCC NTA methodology parallels the treatment of trust structures in NSW assessments — trust-held assets are generally excluded from NTA calculations. ↩

- Division 7A of the Income Tax Assessment Act 1936. Director loans from private companies must be placed on compliant loan agreements (7-year or 25-year terms) to avoid being treated as unfranked dividends. See also ATO guidance on Division 7A and the interaction with construction prequalification financial assessments. ↩

- Olvera Advisory — Counterparty Financial Assessment — olveraadvisors.com. Notes that assessments include analysis of related-party transactions including intra-group loans and contractual commitments. ↩

- Procurement Board Direction PBD-2023-04 — Mandatory Supplier Registration. Six-month transition period; mandatory from 1 July 2024 for all suppliers with total engagement exceeding $150,000 (including GST). ↩

- NSW Procurement Policy Framework — Update History — info.buy.nsw.gov.au. December 2024 update consolidated all current policy settings. PBD 2024-02 introduced local market testing above $7.5M. PBD 2024-01 mandated publication of opportunities above $150K on Buy.NSW by 31 December 2025. ↩

- Procurement Board Direction PBD-2019-03 — Access to Government Construction Procurement Opportunities by Small and Medium Sized Enterprises — arp.nsw.gov.au. Requires agencies to seek at least one SME quote for construction processes up to $1 million. See also PBD-2023-03 raising the direct engagement threshold to $250,000. ↩

- LexisNexis — “Australian Construction Law 2026: Key Reforms by State” — lexisnexis.com. Notes the Building Bill 2024 was shelved in favour of targeted Building Productivity Reforms. ↩